Intelligent Investment

A Quadrant Approach to Commercial Real Estate Investing: Public Equity

By: Dennis Schoenmaker, Ph.D., Randy Zisler, Ph.D. *, Matt Mowell and Michael Leahy

November 5, 2024 5 Minute Read

Executive Summary

Receive EA Insights Directly in your Inbox

- Unlike private real estate with its fixed-income-like returns, Real Estate Investment Trust (REIT) returns are more volatile.

- REIT and small cap stock returns are similar, especially regarding volatility.

- REITs’ total returns are a function of small cap stock returns, unleveraged property returns, and Baa corporate bond returns.

Introduction

This Viewpoint is the fourth in a series that examines the relationship between the CRE quadrants of public debt, private debt, private equity and public equity. Specifically, we will analyze the historic performance of public equity (REITs) in relation to the quadrants.

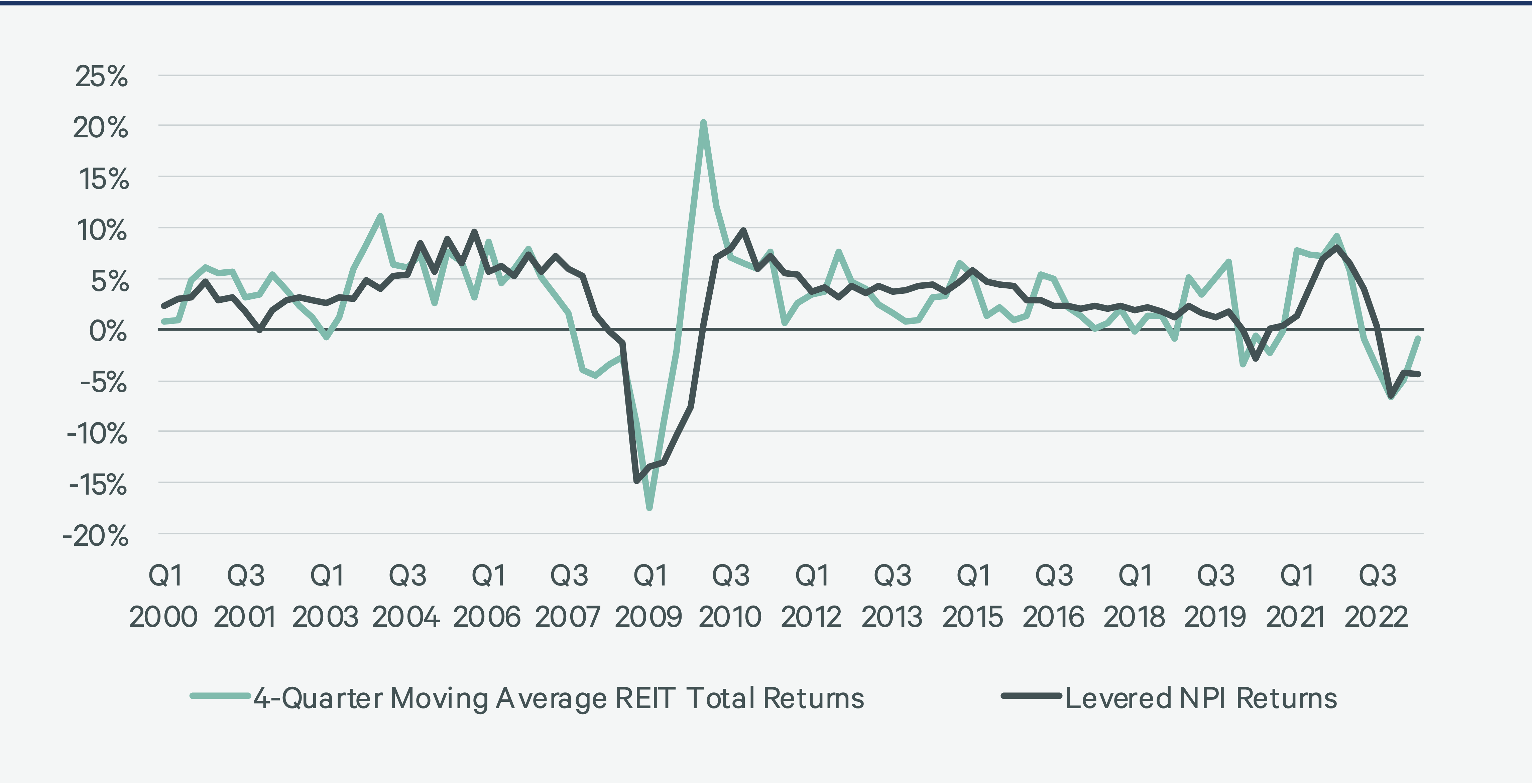

REITs have been a leading indicator of property returns as public market pricing incorporates information faster than backward-looking private markets. REIT returns lead property returns by at least one quarter. REIT returns impound real estate news faster than do property returns.

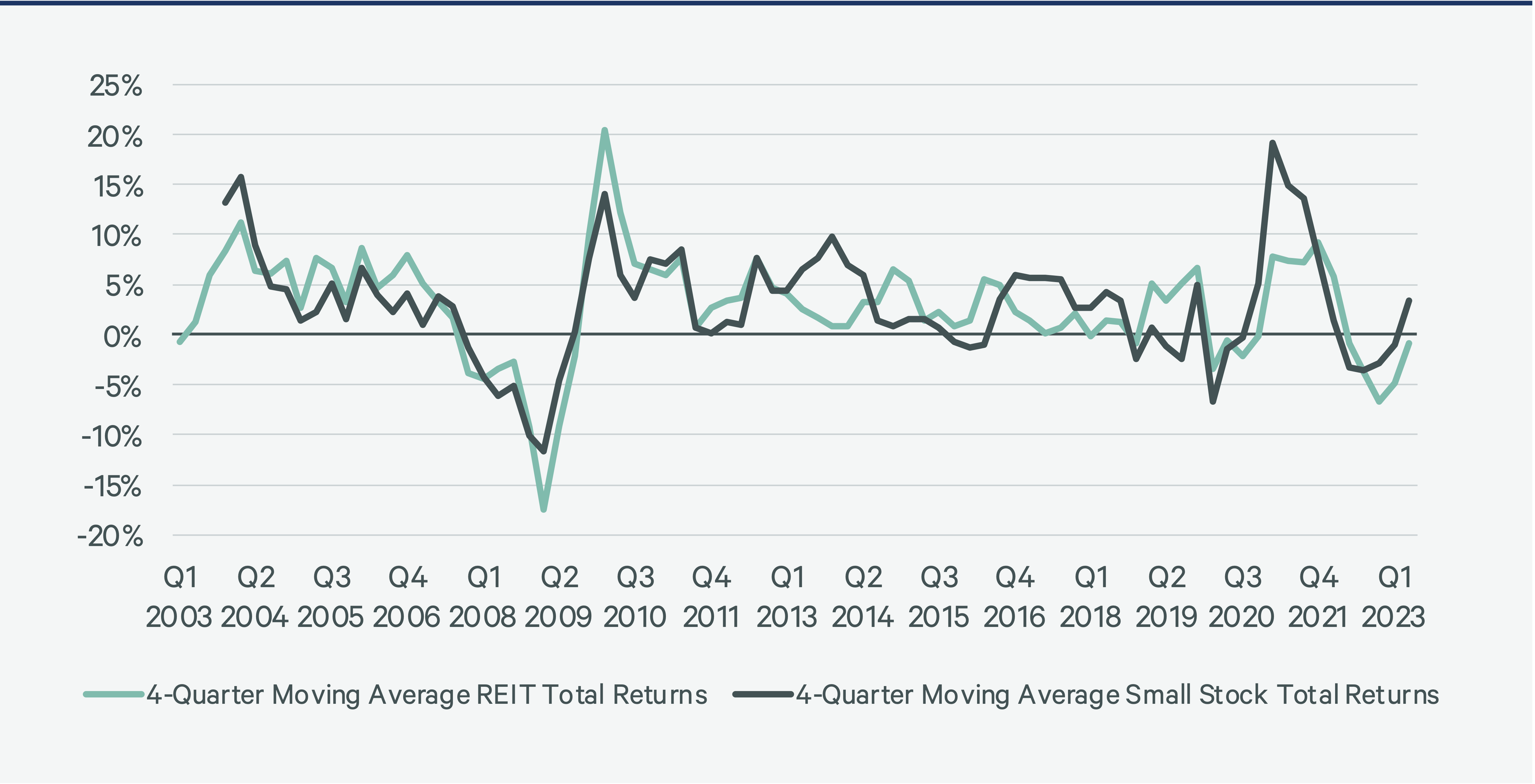

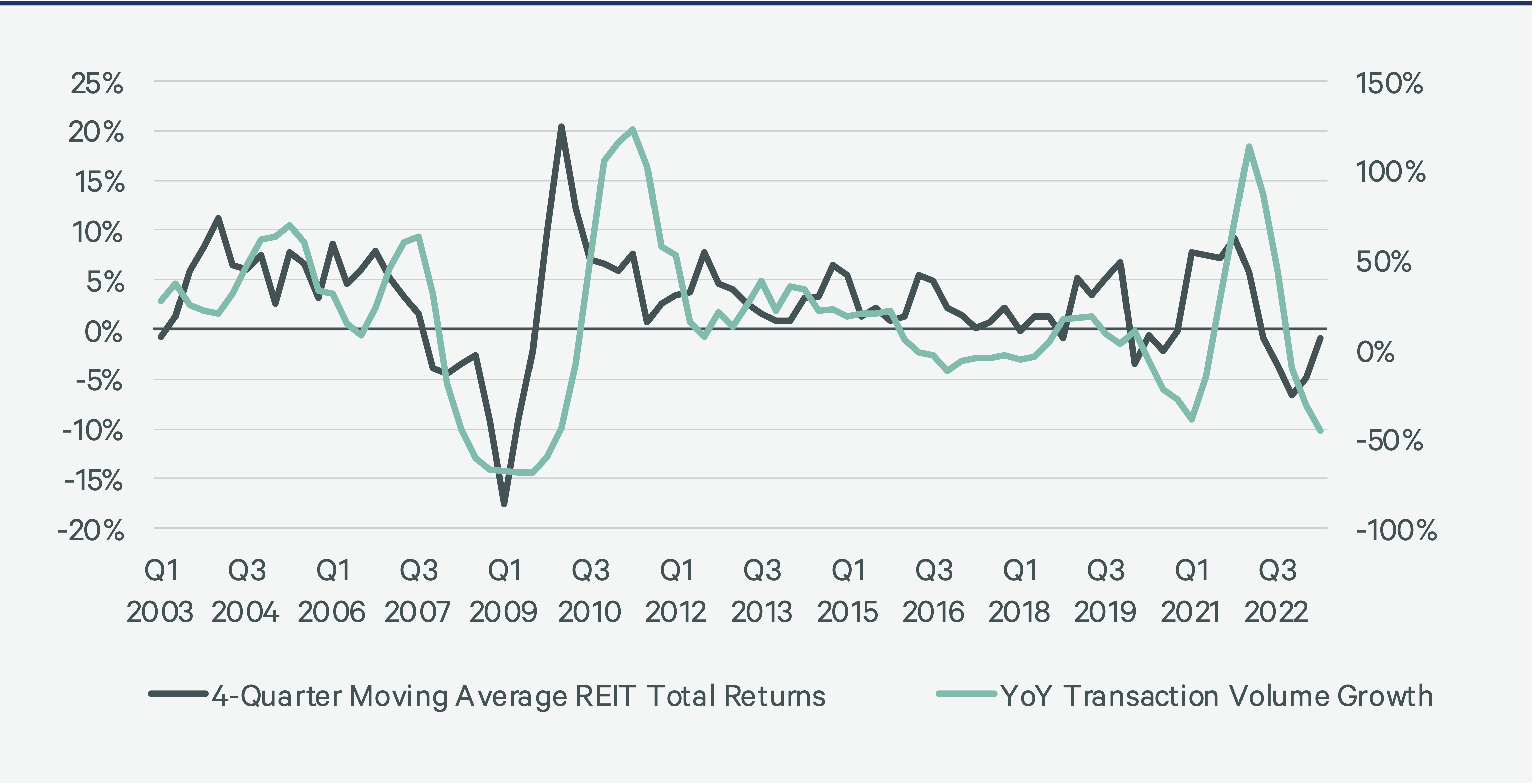

The total returns of REITs and small cap stocks are also highly correlated (Figure 2). In fact, some investors regard equity REITs as a substitute for property. However, it is important to note that this holds true over a longer-term investment horizon, as the return distributions of REITs and property can vary significantly in the short term. Property transactions volume and REIT performance are positively correlated (Figure 3). When REIT investors are pessimistic, property transactions volume declines, impairing price discovery and market efficiency.

Figure 1: Equity REIT and Levered NPI Total Returns (%)

Figure 2: Small Cap Stock and Equity REITs Returns (%)

Figure 3: Moving Average REIT Returns Vs. Transactions Volume Growth (%)

Model

As we show in Figure 2, REITs are highly correlated with small stocks. Therefore, we utilize small stock total returns as our first independent variable. Additionally, we use the total returns on Baa corporate bonds, which captures changes in interest rates and economic conditions. Because past REIT returns are not a good predictor of current REIT returns, we exclude lagged explanatory variables (including lagged REIT returns).

REITs are faster at integrating all information than private CRE. Therefore, lagged REIT returns can help explain property returns. At the same time, property is also a concurrent correlate with REIT performance as stronger brick-and-mortar leasing, occupancy, and NOI growth also bolsters REIT Funds from Operations (FFO). Simply put, common market conditions drive both the REIT and property performance. Although private performance may not be the predominate indicator of REIT returns, we added it as our final independent variable. Adding unlevered NPI returns improves the adjusted R-squared slightly from 63.5% to 69.4%.

Model 1: Equity REIT Returns Explained (Q1 2003-Q2 2023)

|

REIT Total Return |

Coefficients |

|

Small Stocks Total Return |

0.532*** |

|

Unlevered NPI Total Return |

1.105*** |

|

Baa Corporate Bond Total Return |

1.198*** |

|

Constant |

-2.539*** |

|

Observations |

82 |

|

Adjusted R-squared |

0.694 |

|

Durbin-Watson |

2.060 |

Mean Variance Inflation Factor Value = 1.26.

The model explains 69.4% of the variation in equity REIT returns. Explanatory variables include total quarterly returns for small cap stocks, the unleveraged NCREIF property index, and Baa-rated corporate bonds. A one-percentage-point increase in small cap stock returns is associated with a 0.53% increase in REIT returns. REITs behave very much as small cap stocks. When the unleveraged NCREIF Property Index return increases by one percent, REIT returns increase by 1.1%. Baa-rated corporate bond returns play an important role in the cost of capital and are significant contributors to property performance. REITs are no exception, as their assets are primarily properties. A one-percent increase in corporate bond returns is associated with a 1.2% increase in REIT returns.1

Conclusion

The characteristics of private market and public market return data differ in important and material ways that affect risk and public-private analyses. Unlike publicly traded stocks (such as REITs) and some fixed income securities that trade in continuous auction markets, private assets do not have the same level of market liquidity. Private market pricing is backward-looking due to appraisal and other pricing methodologies; these markets react with a lag to public market shocks. That is why the public markets can help us better understand private asset performance.

Moreover, since property returns exhibit serial correlation or smoothing, past property returns can predict (to some degree) future returns. This is not the case with heavily traded stocks like the S&P 500 or public REITs, which exhibit little, if any, serial correlation.

Public markets offer greater transparency and liquidity compared to private markets, where transactions costs tend to be higher, and liquidity is limited. Private returns are serially correlated or smoothed because they are backward-looking. On the other hand, public market prices incorporate information almost instantaneously and are forward-looking. They exhibit near random fluctuations, as theory would suggest. The randomness of public prices does not mean, however, that public markets defy or lack causality. Quite the contrary. Public markets are just more efficient at impounding news; prices fluctuate as if they are statistically random.

Explore Other Viewpoints in This Series

-

Viewpoint | Intelligent Investment

A Quadrant Approach to Commercial Real Estate Investing: Private Equity

February 5, 2025

Property returns exhibit serial correlation, making them partially predictable based on past returns. This needs to be considered when comparing private and public property returns.

-

Viewpoint | Intelligent Investment

A Quadrant Approach to Commercial Real Estate Investing: Private Debt

August 7, 2024

Senior mortgage returns are far more correlated across property types than property investments.

-

Viewpoint | Intelligent Investment

A Quadrant Approach to Commercial Real Estate Investing: Public Debt

July 12, 2024

Commercial mortgage-backed securities (CMBS) allow fixed-income investors to gain exposure to commercial mortgages based on their desired risk tolerance.

-

Viewpoint | Intelligent Investment

A Quadrant Approach to Commercial Real Estate Investing

June 17, 2024

The four primary ways investors can gain exposure to commercial real estate are private equity, public equity, private debt and public debt.

Related Services

CBRE’s trusted specialists in economics, data science, and forecasting at Econometric Advisors deliver the most sought-after analytical real estate re...

- Invest, Finance & Value

Capital Markets

Gain proactive insights and strategies that unlock value, drive returns and enhance outcomes for your real estat...

Contacts

Dennis Schoenmaker, Ph.D.

Executive Director & Principal Economist, CBRE Econometric Advisors