Report | Intelligent Investment

2024 Asia Pacific Real Estate Market Outlook Mid-Year Review

July 30, 2024 15 Minute Read

Executive Summary

Looking for a PDF of this content?

Explore our APAC Online Data Dashboard

CBRE’s 2024 Asia Pacific Real Estate Market Outlook Mid-Year Review looks back at the predictions we made at the beginning of the year and evaluates what we got right, and what we got wrong.

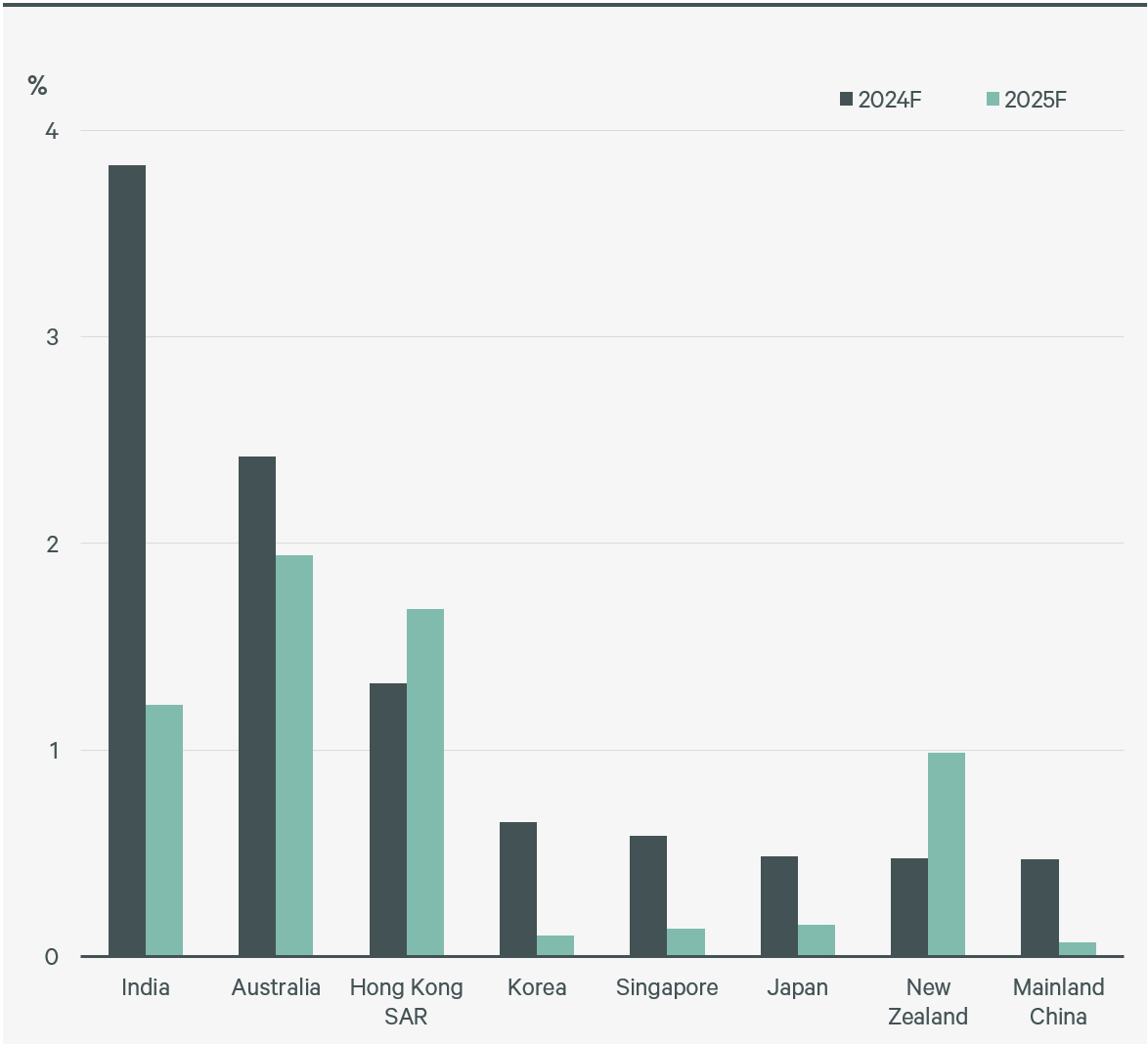

On the economic front, fears of a recession in the U.S. have faded, with the country’s economic strength providing a strong tailwind to many Asian countries’ exports. With the regional employment outlook remaining positive as office-based employment continues to grow, CBRE has upgraded its 2024 Asia Pacific GDP growth forecast to 3.9%. Sluggish growth in mainland China remains the key risk facing the region.

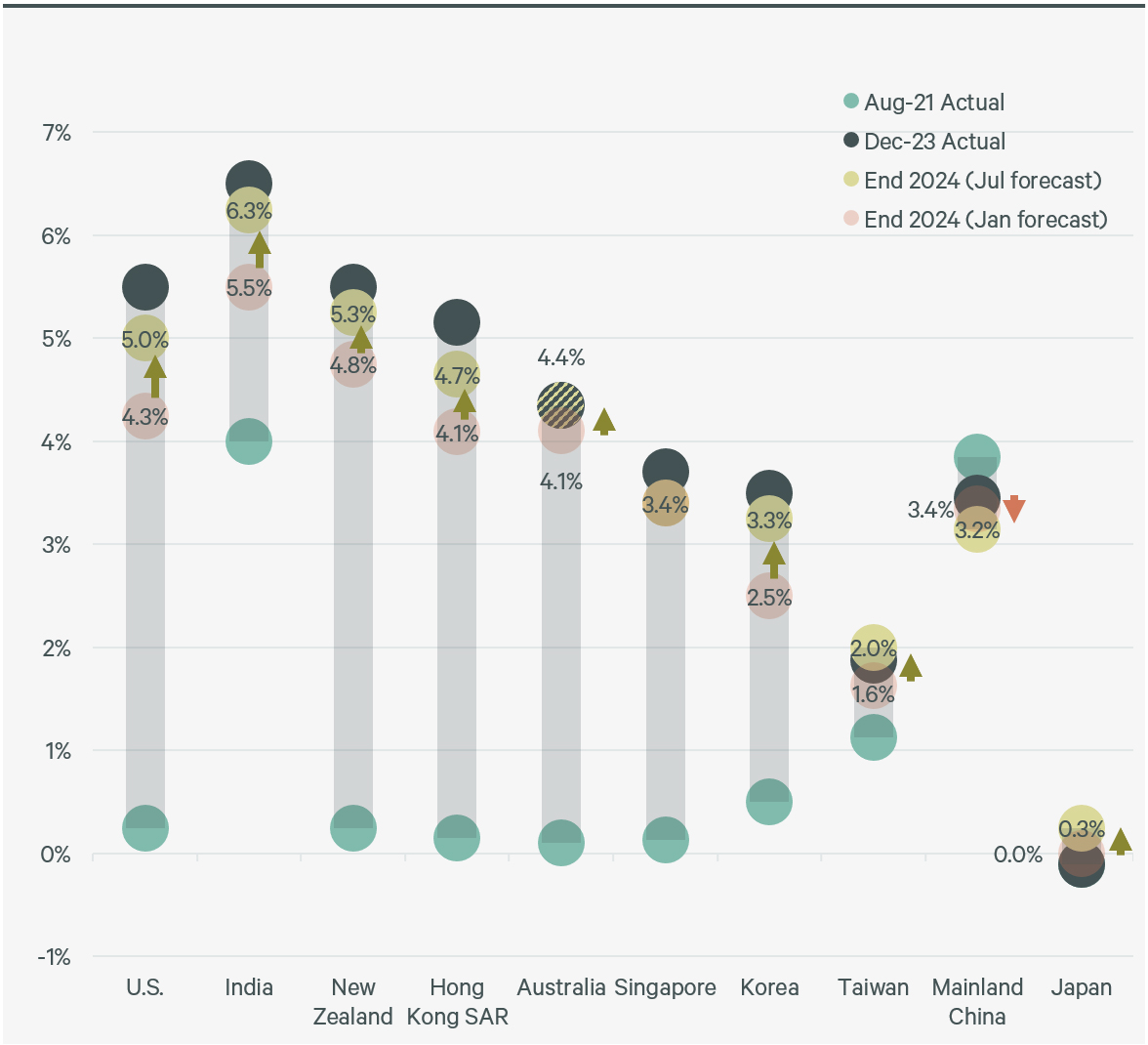

CBRE expects the U.S Federal Reserve to start cutting rates in September as the inflation measure has moved closer to its target. Policy rates across Asia Pacific (ex. mainland China) will end higher than CBRE’s January forecast and are unlikely to return to pre-pandemic levels in the short term.

As in North America and Europe, a full recovery in commercial real estate investment activity has yet to be witnessed in Asia Pacific as expectations for the timing of interest rate cuts are continually pushed back and the rate of repricing has yet to match expectations. CBRE has therefore slightly revised down its full-year investment volume forecast to an increase of 0% to 3%. Reaching this target will be highly dependent on the level of purchasing activity in Japan.

Oversupply continued to impact the Asia Pacific office market in H1 2024, pushing up vacancy to a record high. Cost remains the dominant factor driving renewal and relocation decisions. CBRE’s expectation of full-year growth in gross leasing volume remains unchanged. While rents in most markets saw steady gains in H1 2024, growth is expected to lose momentum or remain stagnant in H2 2024.

Expansionary demand in the retail sector remains resilient, with F&B and sports-related retailers most active. While vacancy in prime shopping precincts has now returned to pre-pandemic levels, CBRE expects retailers to adopt a more cautious approach towards expansion as many have already rebuilt their store networks from pandemic-induced closures. The rental recovery will continue to be driven by prime assets in core locations.

Logistics demand normalised faster than expected in H1 2024, with a preference for renewals over relocations due to high rents and fit-out costs. Despite a mild improvement in leasing activity expected in H2 2024, full-year leasing volume will be weaker than in 2023. With intense competition for tenants set to push up incentives even further, CBRE has downgraded its 2024 regional logistics rental outlook.

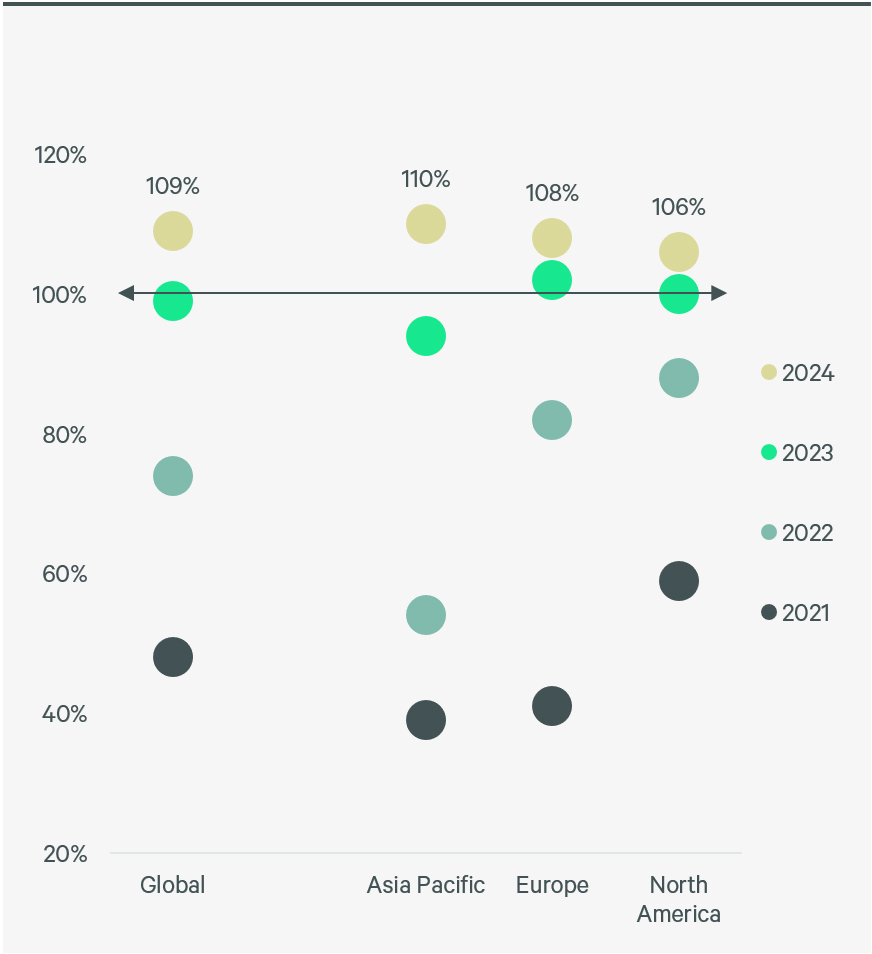

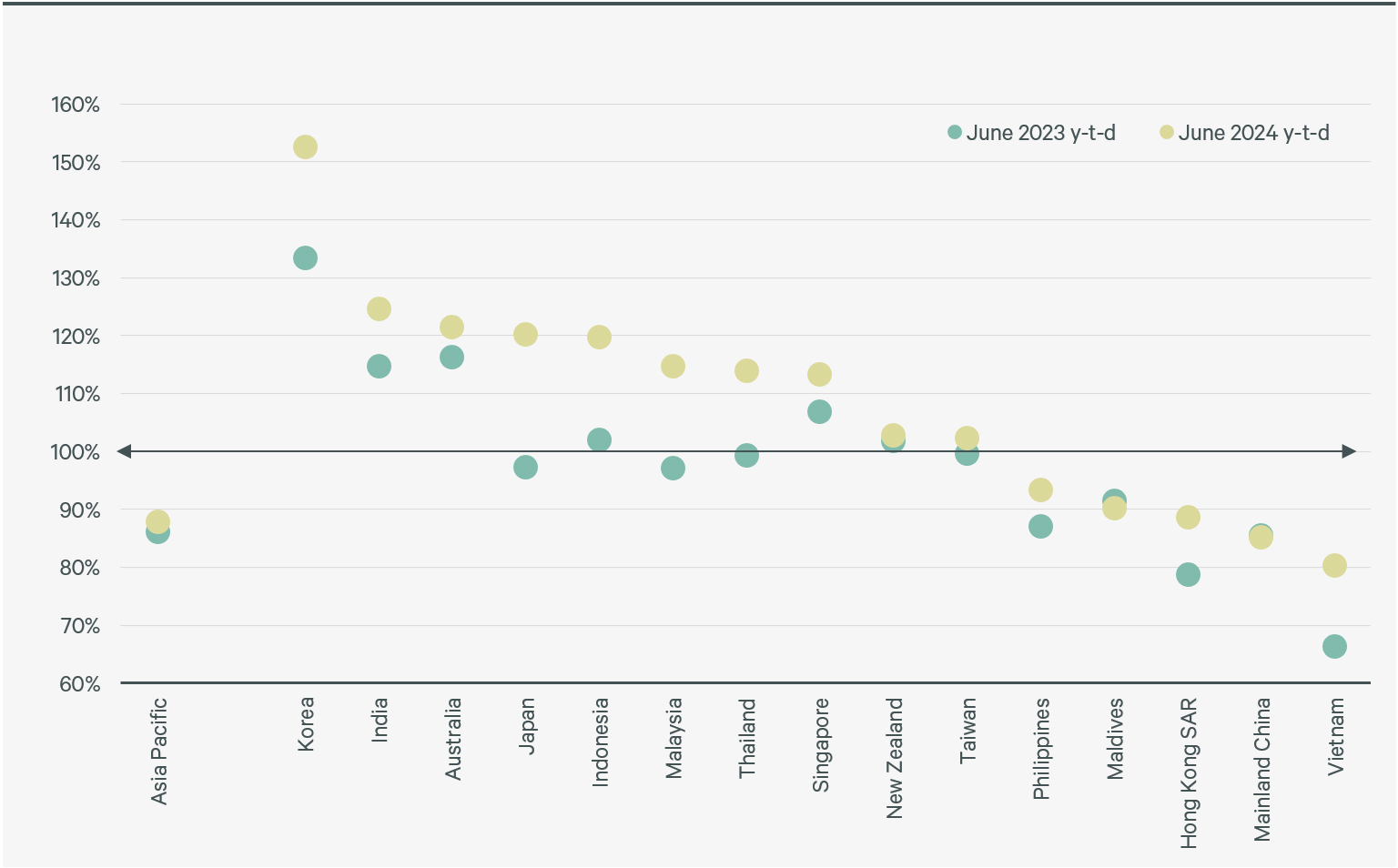

Except for the Maldives, all hotel markets in the region had witnessed y-o-y increases in RevPAR performance as of June 2024 y-t-d. Despite ongoing challenges relating to staffing and aircraft shortages, Asia Pacific has seen significant growth in airline demand in 2024.

Economy

Figure 1: Employment growth in Asia Pacific remains positive in 2024

(Click to enlarge)

Figure 2: Interest rate outlook – rate cut cycle to start later than expected

(Click to enlarge)

Investment

Cap rate expansion to materialise

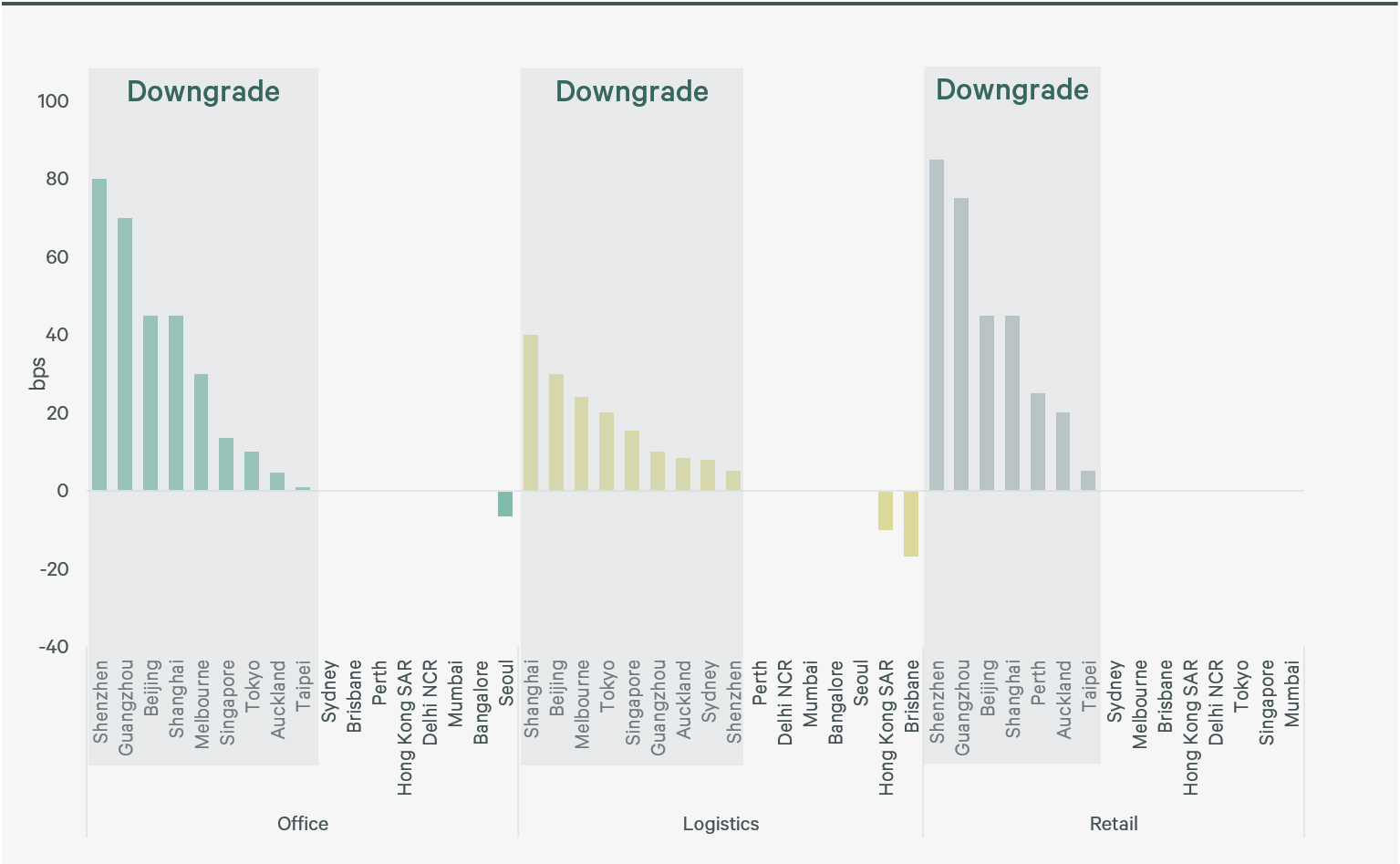

Revised yield forecast- Forecasted 2024 yields in mainland China have seen some of the largest expansion in the region, with Shenzhen reporting upward revisions as high as 85 bps. This is due to expectations of further rental declines and subdued investor sentiment in the coming years.

- Despite some distressed sales, yield expansion in Hong Kong SAR continues to lag the rest of the region.

- On the back of a slight interest rate hike earlier in the year and the possibility of further rate hikes later in 2024, CBRE has revised up its forecast for Tokyo logistics and office yield expansion by 20bps and 10 bps, respectively. This comes as foreign investors adopt a more cautious attitude towards investing in mainstream assets in Japan.

- Evidence of repricing in a large-ticket office deal in Singapore has led CBRE to revise its yield forecast for office upwards by 14bps. The yield forecast for logistics has also been revised upwards as price growth lags rent growth.

- In Australia, yields in the office sector have been revised in anticipation of further expansion, ranging from 12 bps in Sydney to 92 bps in Melbourne, amid repricing observed in recent transactions. Logistics yields have been revised upwards in Sydney and Melbourne and are now set to soften by 25-40 bps in H2 2024.

- Seoul has seen only minor revisions to office yield forecasts for 2024, with projections revised down to 4.45% due to a lack of repricing for recent deals along with possible rate cuts in H2 2024.

Figure 3: Changes to 2024 yield forecast

Source: CBRE Research, July 2024

(Click to view the Asia Pacific Data Dashboard)

Office

Key changes to forecast

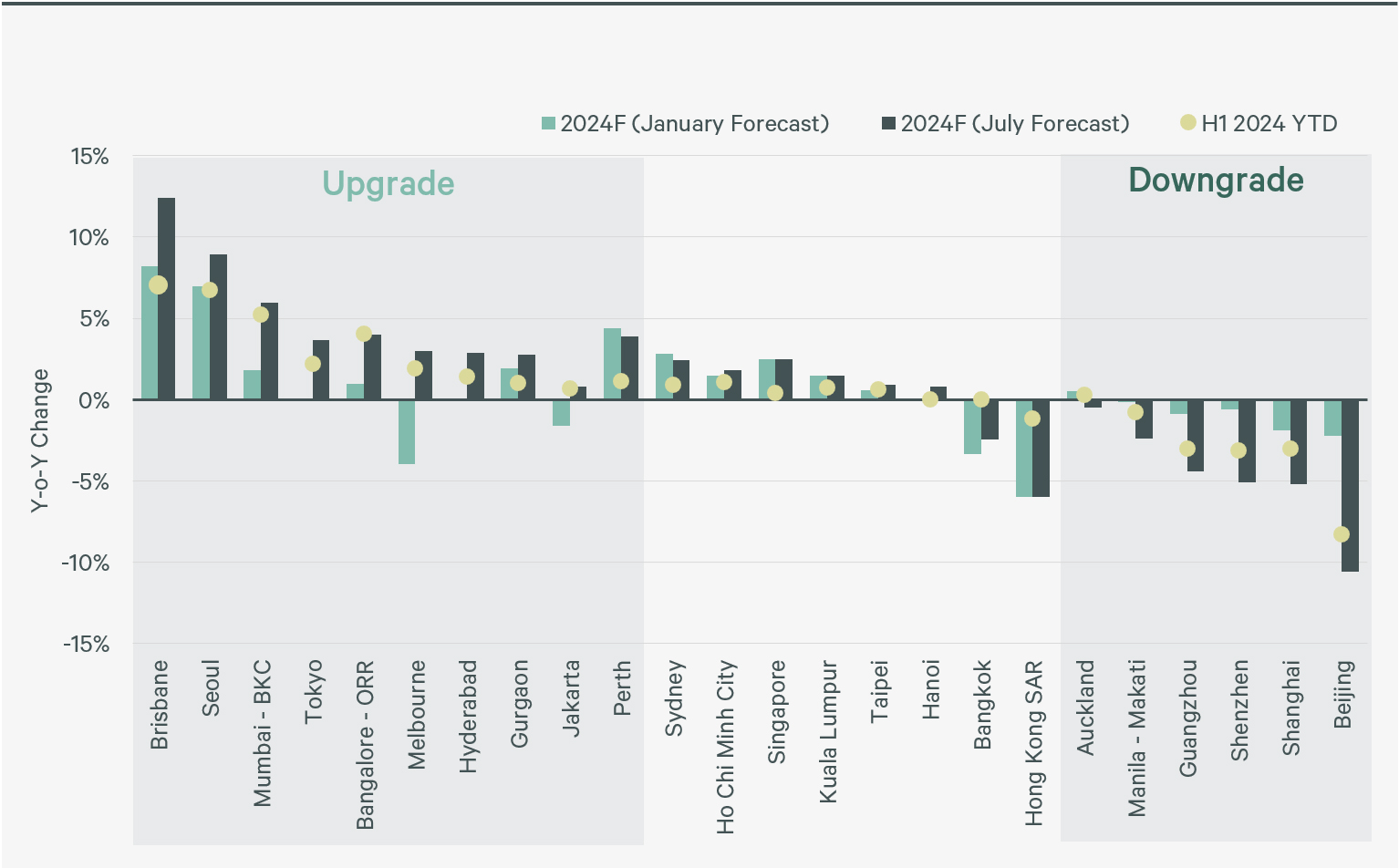

Upgraded- Brisbane and Seoul will remain the main drivers of office rental growth in the region. Tightening availability in both markets has prompted CBRE to raise its forecast for rental growth this year.

- Brisbane continues to report the lowest vacancy of any Australian market. Prime office vacancy will fall into the single digits in H2 2024, paving the way for robust effective rental growth. Rents in Melbourne will bottom out earlier than expected due to stronger leasing activity, although performance will vary across different CBD precincts. However, incentives in Australia will remain high at 30-50%.

- While high pre-commitment rates in new projects and ultra-low vacancy led to rental growth of just under 7% in Seoul in H1 2024, growth may slow in future due to softer leasing sentiment.

- Ongoing flight to quality and expansion by domestic occupiers in existing buildings continues to tighten availability in Tokyo. Landlords of existing buildings are raising rents for existing tenants who lack the CapEx to move. However, upcoming supply in 2025 could force landlords to soften their stance in H2 2024.

- Upbeat leasing sentiment and robust outsourcing activity have pushed up rents for prime core assets in key submarkets in Indian cities, with limited office stock set to ensure further steady growth.

Downgraded

- The rental decline in mainland China tier 1 cities is unlikely to moderate given the significant supply-demand imbalance. Beijing will be the regional laggard as landlords with premium office portfolios join the price war and cut rents to attract tenants. Rents may start to recover in 2027 when supply pressure begins to ease.

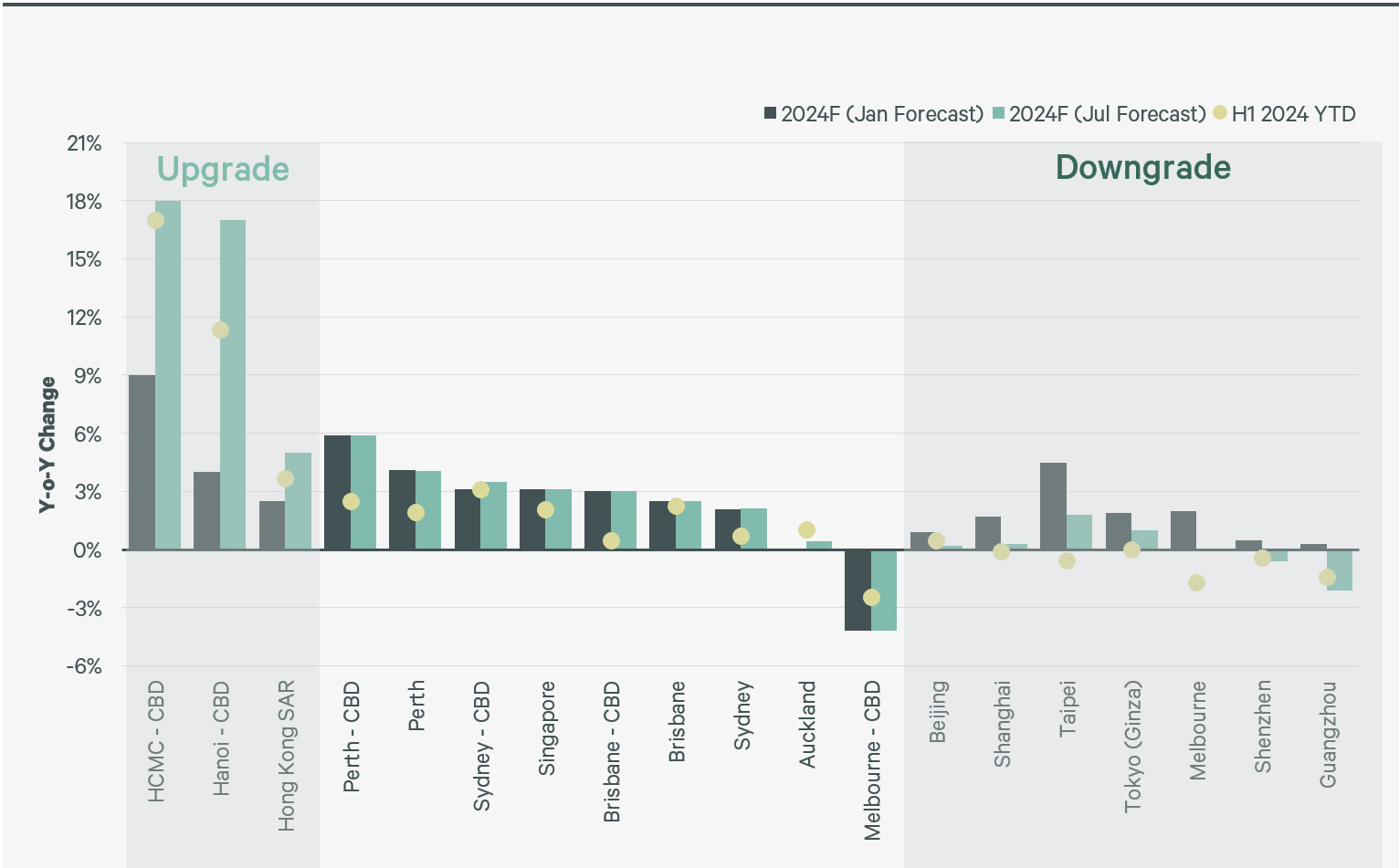

Figure 4: H1 2024 YTD and 2024F Asia Pacific office rental forecast

Source: CBRE Research, July 2024

(Click to view the Asia Pacific Data Dashboard)

Retail

Key changes to forecast

Upgraded- The Ho Chi Minh City and Hanoi CBDs reported record double-digit rental growth in H1 2024 – the strongest of any market – due to the absence of space capable of accommodating demand from the growing number of international brands.

- Hong Kong SAR’s stronger-than-expected rental performance in H1 2024 was driven by demand from mainland Chinese retailers. However, tight vacancy and weakening sales performance have prompted retailers to turn more cautious in recent months, meaning that rental growth in core shopping districts will soften over the remainder of the year.

Downgraded

- With retailers in mainland China looking to operate leaner store networks, downward pressure on rents has intensified as landlords seek to attract and retain reputable tenants.

- Prime CBD retail and regional centres in Melbourne remain the laggards. The rental correction in the prime CBD is due to prolonged construction, while incentives in regional centres have edged up as retailers grapple with softening sales growth and prolonged inflationary cost pressure.

- Rents in Taipei reached the bottom in H1 2024, two quarters later than CBRE’s forecast. Retailers’ selective approach will ensure the rental recovery remains modest despite strong local consumption demand and tourist spending.

Figure 5: H1 2024 YTD and 2024F Asia Pacific retail rental forecast

Source: CBRE Research, July 2024.

(Click to view the Asia Pacific Data Dashboard)

Logistics

Key changes to forecast

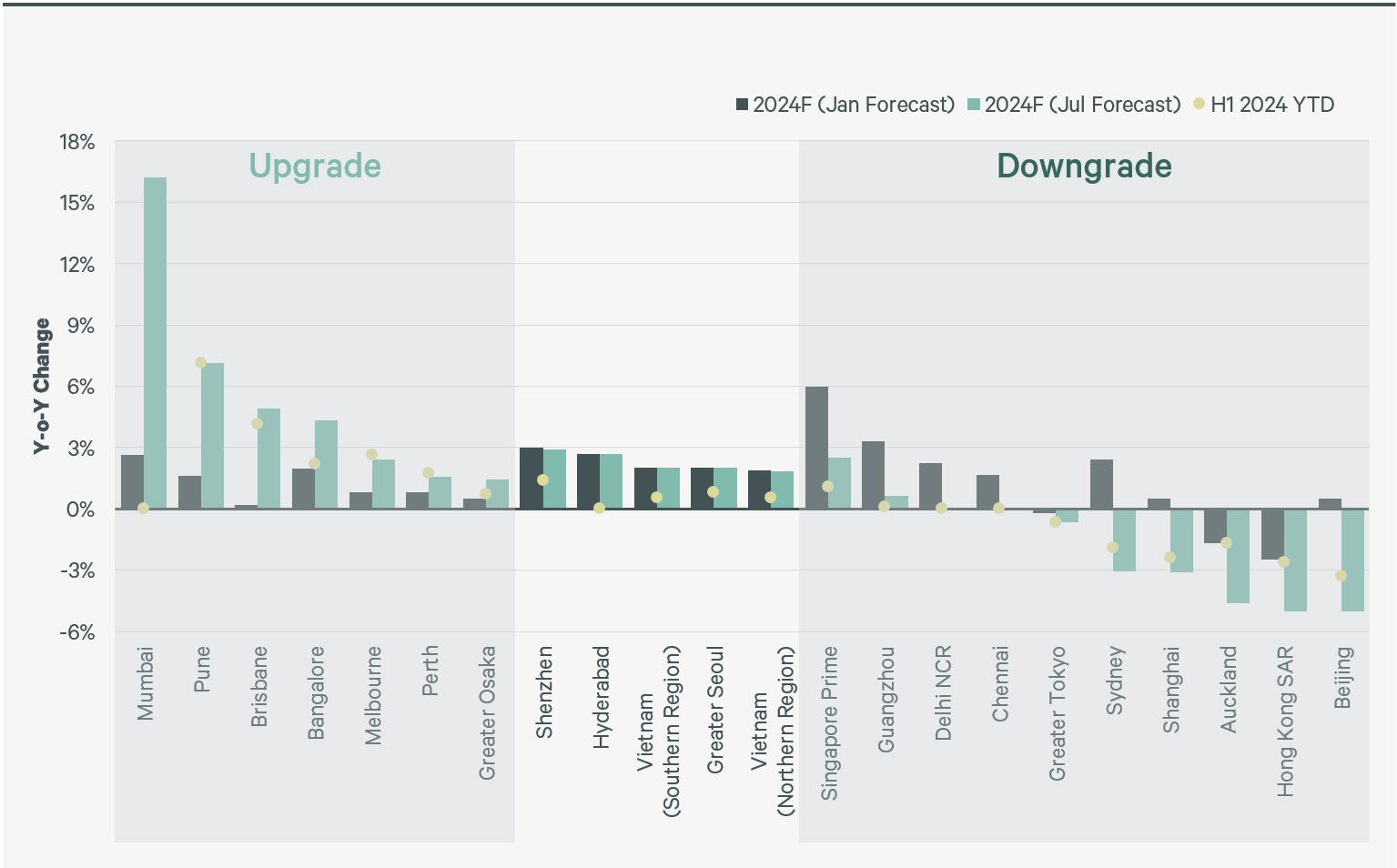

Upgraded- Mumbai and Pune are set to lead logistics rental growth in Asia Pacific over full-year 2024. Growth will be underpinned by the completion of well-located premium grade assets commanding higher rents.

- Rental growth in Brisbane and Melbourne has been driven by selected precincts. Rising incentives will offset the increase in face rents in H2 2024.

Downgraded

- Room for further rental growth in Singapore Prime is limited as occupiers turn more resistant to high rents. Some have adopted a wait and see approach due to the ample supply pipeline in 2025.

- A slowdown in demand in Sydney coupled with rising availability from shadow space and new supply has pushed up incentives. CBRE has downgraded its full-year rental forecast to a 3% decline, making it the first Australian market to reach the peak of the rental cycle.

- Except for Shenzhen, downward pressure on rents in markets in Greater China has intensified. The rental decline in Beijing and Shanghai will continue in the medium term with vacancy having risen to decade-highs amid an ongoing downsizing trend along with cost-saving relocations to self-built warehouses or facilities in satellite cities. Rents in Hong Kong SAR will remain sluggish due to weak near-term economic prospects.

Figure 6: H1 2024 YTD and 2024F Asia Pacific logistics rental forecast

Source: CBRE Research, July 2024.

(Click to view the Asia Pacific Data Dashboard)

Hotels

Figure 7: Airport throughflow by region (by year) as a % of 2019 levels

(Click to enlarge)

Figure 8: RevPAR - Asia Pacific (% change vs June 2019 y-t-d)

(Click to enlarge)

2024 Asia Pacific Mid-Year Outlook Event

Related Mid-Year Market Outlook Insights

- Intelligent Investment

India Mid-Year Market Outlook 2024-25

This analysis evaluates the progress made on those projections during H1 FY2024-25, i.e., between April and September 2024, and recalibrates them for the remaining months of the financial year.

- Intelligent Investment

2024 China Real Estate Market Outlook Mid-year Review

On the economic front, GDP grew by 5.0% y-o-y in H1 2024, underpinned by resilient exports and the rebound in manufacturing investment.

- Intelligent Investment

UK Mid Year Market Outlook 2024

2024 started with a renewed sense of optimism. While there was evidence of improved positivity with a pick-up in retail sales, consumer confidence, and a return to economic growth, there have been some less encouraging signs.

- Intelligent Investment

Taiwan Market Outlook Mid-Year Review 2024

Despite ongoing geopolitical risk, Taiwan’s GDP is forecasted to reach 3.9% y-o-y in 2024, underpinned by solid household consumption.

Asia Pacific Real Estate Market Data Dashboard

Explore dynamic real estate data across all sectors

Use the Dashboard Data Subscription Service

Research Contacts

Business Contacts

Greg Hyland

Head of Capital Markets, Asia Pacific

Luke Moffat

Head of Advisory & Transaction Services, Asia Pacific

Danny Mohr

Head of Valuation & Advisory Services, Asia and Head of International Valuations, Asia Pacific

Richard Stevenson

Managing Director, Head of Office Occupier, Asia Pacific

Vivek Kaul

Managing Director, Head of Retail, Advisory & Transaction Services, Asia

Michael Bowens

Managing Director, Head of Industrial & Logistics, Advisory & Transactions Services, Asia Pacific